Can you launch a lending business in 60 secs for free? Introducing Global Lending

Ecosystem (GLENZY).

The concept of finance and technology was introduced to the world years ago and

it has been booming since then. When you merge these two separate yet extremely

strong entities, it builds up a robust platform that can make you millions or

maybe billions. With the world turning digital and preferring the hassle-free

method of payments, loans, deposits and all monetary transactions, fintech's

future is bright. We enable you to make that dream a reality!

Is the Fintech industry here to stay? Fintech Growth cycle

The fintech industry is expected to continue growing in the coming years. There

are a few key factors driving this growth:

-

Increased adoption of digital technologies: As more consumers and

businesses rely on digital technologies for their financial needs,

fintech companies are well-positioned to meet this demand.

-

Changing consumer preferences: Consumers are becoming increasingly

comfortable with using digital platforms for financial services, which

has led to a rise in fintech usage.

-

Regulatory changes: Governments around the world are implementing

regulations to support the growth of fintech companies, which has helped

to create a more favourable environment for these firms to operate.

-

The rise of open banking: With the rise of open banking, consumers are

able to share their financial data with third parties, which has led to

an increase in the number of fintech companies offering new and

innovative services.

-

The increasing use of Artificial Intelligence and Machine Learning: By

implementing AI and ML, fintech companies are able to offer more

personalized services, such as financial advice and fraud detection,

making the experience easier for the consumer.

Let's talk about the Tech in Fintech

The Tech in Fintech makes hours of laborious work into a simple and systematic

system, therefore, increasing efficiency and accuracy at the same time.

Technology plays a critical role in the lending process by automating and

streamlining many of the traditionally manual tasks that were previously

required. For example, online lending platforms use algorithms and data analysis

to assess a borrower's creditworthiness and determine the terms of a loan, such

as the interest rate and repayment schedule. This allows for faster loan

approvals and lower interest rates for borrowers. Additionally, technology can

be used to verify a borrower's identity and income and to securely transfer

funds between the lender and the borrower. Overall, technology enables fintech

companies to offer more efficient and convenient lending services to consumers

and small businesses.

The 3 important lending pillars in the lending process

- Lenders

- Dealers

- Borrowers

-

Lenders are financial institutions or

individuals who provide loans to borrowers. They can be traditional

banks, credit unions, online lenders, NBFA or other types of financial

institutions. Lenders assess the creditworthiness of borrowers and

determine the terms of the loan, such as the interest rate and repayment

schedule.

-

Borrowers are the individuals or

entities that apply for and receive loans from lenders. They may be

individuals seeking personal loans, or businesses looking for funding to

expand their operations. Borrowers are typically required to provide

information about their income, assets, and credit history in order to

qualify for a loan.

-

Dealers are intermediaries between

lenders and borrowers. They may connect borrowers with lenders, and help

to facilitate the loan process. They can be independent agents,

financial institutions like banks, or online platforms that match

borrowers and lenders. Dealers can also provide additional services such

as credit counselling or loan origination.

The role of dealers in the lending business is immensely inclining as a

lot of consumers prefer EMI and loan options directly from the stores

rather than opting for a long route of reaching out to a financial

institution, getting a loan and then buying the product from the store.

The Process of a money lending procedure in fintech

-

Application: The borrower submits an online application,

including personal and financial information. Fintech companies

typically use digital channels like their website or mobile app to make

the process more convenient for the borrowers.

-

Eligibility check: The lender reviews the application and

checks the borrower's creditworthiness and eligibility for the loan.

They use various digital tools such as alternative data and machine

learning algorithms to make a decision.

-

Approval/Denial: The lender approves or denies the loan

application based on their internal policies and guidelines. Fintech

companies tend to have more lenient policies and use more advanced

technology that allows them to make faster decisions compared to

traditional financial institutions.

-

Document submission: If approved, the borrower submits

additional documentation, such as proof of income and identification.

Fintech companies can use digital tools such as e-signatures and

automated document verification to make this process more efficient.

-

Funding: If approved, the loan is funded and the borrower

receives the funds. Fintech companies can use digital channels such as

mobile wallets and bank transfers to disburse the funds.

-

Repayment: The borrower makes regular payments to the lender

until the loan is fully repaid. Fintech companies can use digital

channels like recurring payments and automatic payments to make the

repayment process more convenient for the borrower.

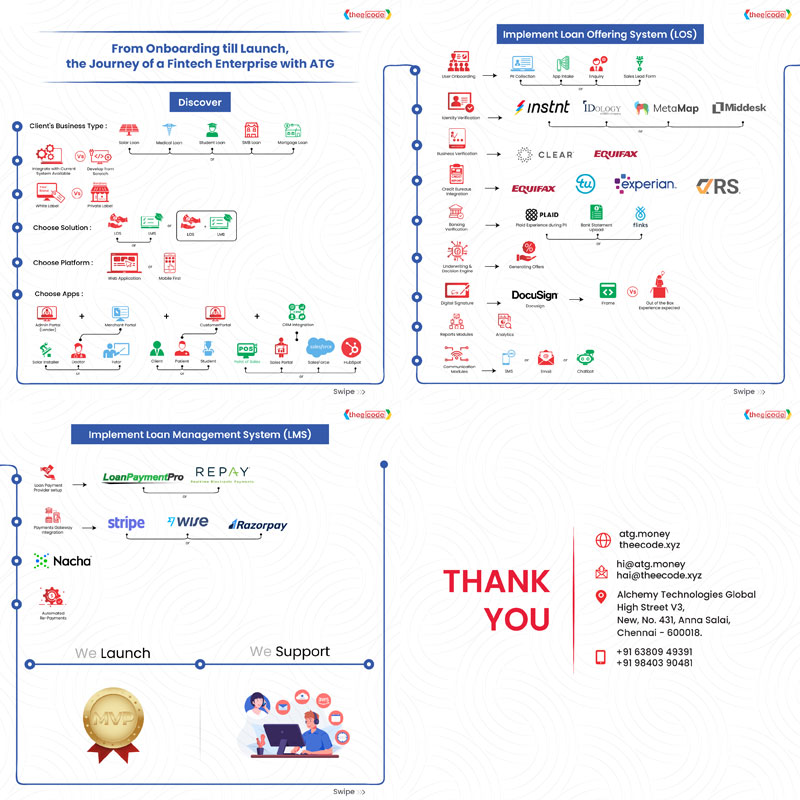

How to streamline the entire lending process in less than 60 secs?

As a fintech company, structuring and initialising the entire lending process

from top to down can be achieved in two ways, either hiring a separate in-house

team for product development or hiring a third-party company for developing the

entire functional software. It is difficult to arrive at a “ONE SIZE FITS ALL”

product with such a sublime process as every client has their own customisation

and requirements resulting in the entire process taking a huge amount of time

and money. Theecode cracked the code for introducing “Embedded Lending Framework

(GLENZY)” which is a full fletched lending process configuration delivered to you

in less than 60 secs. It's a sandbox for every user to experience the usual

format of the lending process and can be used for trials and actual lending

purposes as well. GLENZY will enable you to kickstart your leading business without

any hassle for free in less than 60 secs. IT'S TRUE! We are focusing on building

a revolutionary product to cater to the high demand in the fintech industry

which fits every requirement for a seamless lending process portal. We are

envisioning going forward as a product company delivering you coherent and

smooth tech along with focusing on personalisation and custom-made changes for

your enterprise.

Configurable lending solutions comprising in our GLENZY

-

Theecode have spent months developing a perfect lending solution for

your business. Whether you are a lender or a dealer we have everything

intricately design the product for you. These are the 3 lending

solutions we provide you through enabler.

-

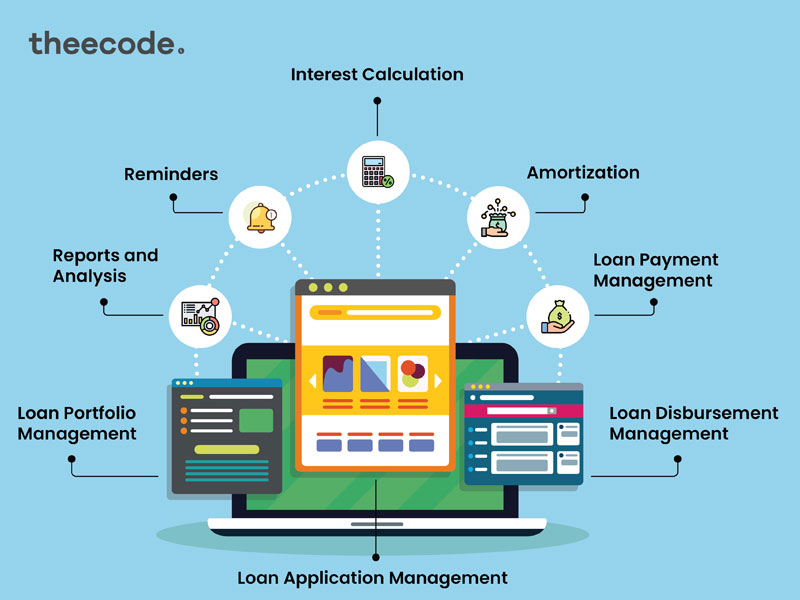

Our Loan Origination System (LOS) is a

software application that automates the process of a loan application,

underwriting, and approval for the borrower. It typically includes

features such as online application forms, credit score checks, document

management, and electronic signature capabilities all in one place. Our

systems can also integrate with other systems, such as credit reporting

agencies and appraisal management systems, to provide a complete view of

the loan application process.

- With Loan Management System (LMS), you

can automate and streamlines the process of loan origination,

underwriting, servicing, and collection for the lender. It typically

includes features such as credit analysis, document management, workflow

management, and reporting. An LMS can be used by financial institutions,

such as banks and credit unions, as well as by non-traditional lenders,

such as peer-to-peer lending platforms. Our system is here to help

organizations manage their loan portfolios more efficiently and

effectively, while also reducing the risk of fraud and compliance

violations.

-

Our Decision Engine (DE) are software

systems that use a combination of data, algorithms, and rules to analyze

information and make decisions. They can be used in a variety of

applications such as business intelligence, fraud detection, and

automated systems. DEs can be rule-based, where decisions are made based

on a set of predefined rules, or more advanced, using techniques such as

machine learning to make predictions and decisions.

-

With a combination of all the three leading lending solution

requirements, you are set to go and test your lending model for free and

if you need any specific alteration and specification, our highly

trained tech comes to your rescue and delivers your wishes like a genie

but not

only limited to 3 wishes. We are building an experience of a high-tech

solution product followed by customisation delivered as a service.